Research paper

3 min

Does value’s comeback mark the end of the decade-long ‘party’?

“It is equally beyond doubt that every speculative mania which has run its course of folly and disaster has derived its original impulse from cheap money.”

This quote is attributable to The Economist magazine. That veritable publication was founded in 1843 and although you might think the quote is from a recent edition, it actually first appeared in 1858 – over 150 years ago! Even if the dates are a little out, it is clear that “cheap money” and its consequences have been around for a long time.

However, today the era of cheap money (frankly, free money in most places around the world) has come to an end. Judging by some of the rather violent movements in many markets across many different asset classes, you could probably say an ‘abrupt’ end! Just as The Economist wrote over 150 years ago, “folly and disaster” have struck at a vast range of “speculative mania”.

It is not surprising that when cheap money starts to be removed, most asset prices begin to fall and all sorts of speculative mania comes unstuck. Or as the Oracle of Omaha put it: “You only learn who has been swimming naked when the tide goes out.”* The Australian equity market (ASX/S&P 300 total return) fell 12.2% for the June quarter. This is the worst quarter since the COVID quarter of March 2020 when the Australian market fell over 20% (of course, the market recovered all of that by the end of 2020). However, when compared to global markets since the downturn in early January 2022, our market has fared relatively well.** This is largely down to composition: our tech sector is relatively small (particularly compared to the US), and we are well represented in resource companies, including energy, which have done well (for a variety of reasons, including the war in Ukraine).

Even in Australia, there has been some first class folly and disaster. Take the ‘buy now pay later’ (BNPL) sector. This was one of the ‘hottest’ sectors at the peak of cheap money, with some eye-watering valuations attributed to companies, most of which had never made a dollar of profit. In Australia, the largest BNPL company, Afterpay, was briefly a top 20 company before it was taken over by an American fintech. As it was a scrip deal, investors have still suffered substantial losses unless they were particularly nimble and sold out. Another large Australian BNPL company was ZIP. The ZIP share price peaked at over $14 (implying a market capitalisation of around $10 billion) in early 2021 and today trades around 50c, a staggering fall of over 90% in less than 18 months.

While the ‘war stories’ from the BNPL sector are enlightening, to be fair they are at the extreme end. However, the valuation dispersion has filtered down into many less esoteric parts of our equity market. For example, Woolworths, the leading consumer staples company in our market, traded on a price earnings ratio (PE) of over 30x on what were arguably COVID-inflated earnings. Similarly for Wesfarmers, which owns the highly successful Bunnings hardware chain. These are fine, generally well run businesses, but the multiples investors were prepared to pay for them were extremely high by historical standards. The refrain, at the time, was that interest rates were low, which they clearly were. What some investors failed to even countenance was that rates may rise one day.

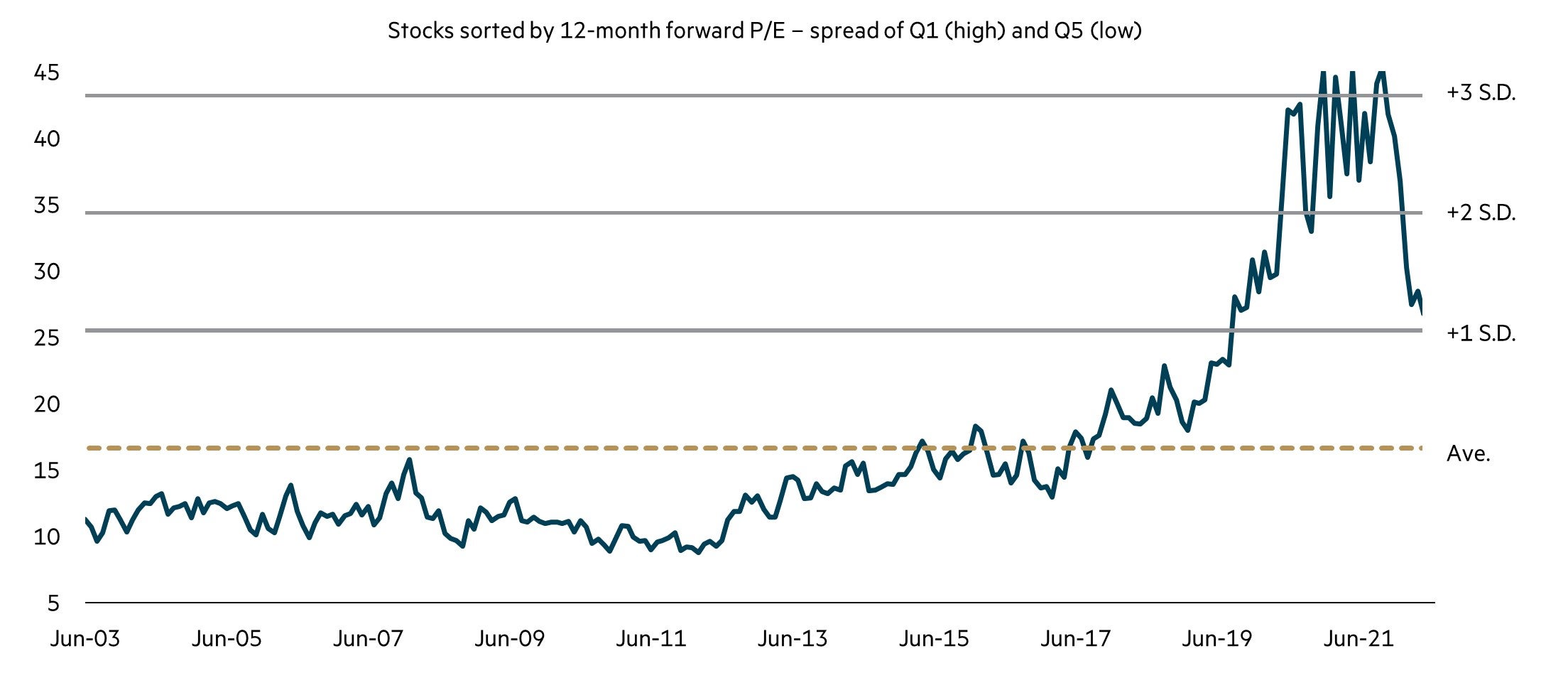

Despite the obvious derating of many of the high-flying growth stocks, we still believe there is a fair bit more to go. This is largely down to the extreme starting position. Depending on which measure you use, at the peak, the highest rated stocks were more than three standard deviations more expensive relative to their lowly rated peers. For example, as the chart suggests, the valuation dispersion for the industrial stocks (excluding financials) is still around one standard deviation above history. Also, after spending such a long time so far above average, it would not be surprising if the situation flipped and the highly rated stocks traded below long-term averages for a period of time.

Multiple dispersion coming back but still wide

Universe is the ASX200 industrials ex-Financials. Note: Quintile next twelve months (NTM) P/E is based on a 40% trimmed mean. Source: Goldman Sachs, data to June 2022

In addition to the withdrawal of cheap money, this particular episode of folly and disaster has been aided by a whiff of stagflation. While the concept of stagflation is reasonably well understood (a period of low growth but high inflation), unfortunately, there is no widely accepted definition.

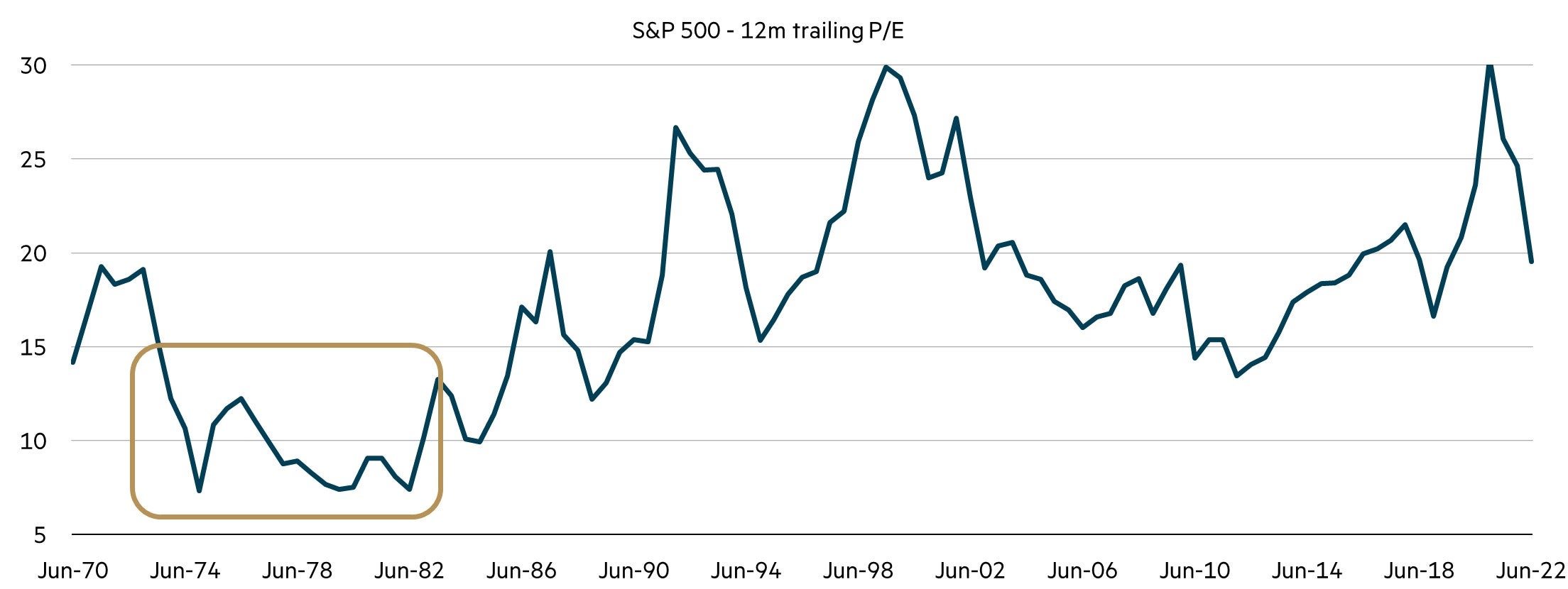

While stagflation will undoubtedly have human costs in terms of lives and livelihoods, our job is to examine stagflation in the context of the impact on equity markets. It is quite clear when looking at returns, particularly real returns, of the equity markets in the late 1970s (the last period of sustained stagflation) that they were particularly unattractive. While no two time periods are ever identical (numerous commentators have argued things are different today: for example, unemployment is much lower), it is instructive to look at what happened to equity markets.

The chart highlights the US trailing PE over the past 50 years, with the stagflation period highlighted. It uses US data as the Australian equity market was dominated by resource stocks back in the 1970s.

Stagflation – limited recent history: significant PE derating seems a likely outcome

Source: Bloomberg, data to June 2022

Clearly, the US market endured a significant derating during the stagflation of the 1970s and early 1980s. The US market suffered a 10 point PE fall (from almost 20 times to under 10 times). Without being too bearish, it is worth noting that this time around the US market started with a PE of around 30x, a similar level to where it started before the so called ’Tech Wreck’ in early 2000! Largely as a result of this PE derating, value stocks did significantly better than growth stocks during the period of stagflation.

Investors will have their own views as to the likelihood of a period of stagflation. Frankly, it is not something anyone would wish for! However, if that scenario eventuates, history suggests that having a portfolio of reasonably priced value stocks is likely to fare far better than a portfolio of expensive growth stocks.

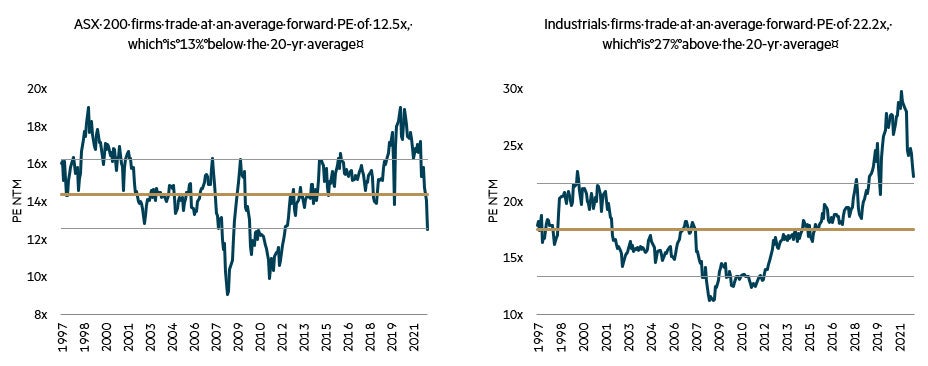

Our portfolios have enjoyed a very strong period of relative performance.*** With the declines in the market, the PE for the Australian market as a whole now looks back in line with historical averages. However, given the wide valuation dispersion that still exists in the Australian market, we remain confident our value style will continue to deliver as the dispersion narrows further, particularly if stagflation eventuates.

Australian market PE broadly in line with historical averages: industrials still expensive

Source: Goldman Sachs, data to June 2022

With the end of the era of cheap money and the potential for a period of stagflation, the Australian equity market has clearly de-rated. However, that market PE still conceals a vast discrepancy between banks and resources on relatively modest PEs (resources as earnings are high reflecting favourable commodity prices and bank share prices seem to be pricing in a potential recession) and relatively high-priced industrials. From here, our concerns are as much focused on the sustainability of the E (i.e. the earnings) as the PE (the multiple you pay for those earnings). In our assessment, the risk to the E lies in the downside for most companies, and we believe returns will be fairly modest over the next period.

* Warren Buffet, Berkshire Hathaway Letter to Shareholders, February 2003

** From 3 January 2022 to 30 June 2022 in AUD terms, MSCI World (Total Return) returned -15.7%, MSCI AC World (Total Return) returned -15.4% and S&P/ASX 300 (Total Return) returned -10.4%.

*** Performance relates to the 12 months to 30 June 2022 and is relative to the index (ASX/S&P 300 total return). Past performance is not a reliable indicator of future performance.

Disclaimer

This information was prepared and issued by Maple-Brown Abbott Ltd ABN 73 001 208 564, Australian Financial Service Licence No. 237296 (“MBA”). This information must not be reproduced or transmitted in any form without the prior written consent of MBA. This information does not constitute investment advice or an investment recommendation of any kind and should not be relied upon as such. This information is general information only and it does not have regard to any person’s investment objectives, financial situation or needs. Before making any investment decision, you should seek independent investment, legal, tax, accounting or other professional advice as appropriate. Past performance is not a reliable indicator of future performance. Any comments about investments are not a recommendation to buy, sell or hold. Any views expressed on individual stocks or other investments, or any forecasts or estimates, are point in time views and may be based on certain assumptions and qualifications not set out in part or in full in this information. The views and opinions contained herein are those of the authors as at the date of publication and are subject to change due to market and other conditions. Such views and opinions may not necessarily represent those expressed or reflected in other MBA communications, strategies or funds. Information derived from sources is believed to be accurate, however such information has not been independently verified and may be subject to assumptions and qualifications compiled by the relevant source and this information does not purport to provide a complete description of all or any such assumptions and qualifications. To the extent permitted by law, neither MBA, nor any of its related parties, directors or employees, make any representation or warranty as to the accuracy, completeness, reasonableness or reliability of the information contained herein, or accept liability or responsibility for any losses, whether direct, indirect or consequential, relating to, or arising from, the use or reliance on any part of this information.

Interested in investing with us?

We are a disciplined Australian equities value manager that has been managing Australian equities since we were established in 1984. Over time we have made refinements to our investment process, however our commitment to value investing remains unchanged.