Article

10 min

Taking shelter from inflation

This article was written by Andrew Maple-Brown and Steve Kempler and was first published on Livewire on 8 February 2022.

We have been perplexed by the relative and absolute underperformance of toll roads globally. This is when road volumes in many parts of the world have returned to normal. Just as puzzling is the fact that airports, where volumes are still down significantly and expect recovery to pre-COVID passenger levels to be several years away, are outperforming toll roads. But fundamentals and stock-picking are starting to matter, and herein we believe are the opportunities.

Two years ago, the world bleakly acknowledged the emerging COVID-19 pandemic before lockdowns and mobility restrictions significantly impacted peoples’ ability and appetite for travel, both for work and leisure, domestically and abroad.

This impact was most stark for airports, where volumes completely dried up – in some cases down more than 99% –and many national borders were closed. Toll road concessions were also impacted. Within the sector, restrictions and reduced mobility demand were more evident on roads that relied on commuter (and airport) traffic, including managed lanes built to relieve congestion on existing roads on the same travel corridor. Traffic volumes on such assets took the bigger dives relative to other toll roads as workers and businesses rapidly transitioned to a ‘work from home’ (WFH) approach in the first half of 2020. We also saw parents home-schooling children and shopping and social activities significantly curtailed.

At the time, investors were naturally asking questions like: How long would it take for traffic to return to the pre-virus trend line? What trajectory would toll growth now take? How would long-term traffic growth be impacted by WFH?

The downside risks of prolonged or permanent WFH impacts had to be balanced with upside risks from a shift from public transport to cars and a rapid shift to ecommerce and just-in-time deliveries changing the vehicle mix towards higher tariff commercial and heavy vehicle traffic. Looking out further, it was also important to consider the hastening longer-term tailwind of technology, greater ride sharing and the increasing penetration of electric and, potentially, autonomous vehicles.

We approached these questions and concerns from a top-down and bottom-up perspective. From the top down, we made estimates guided by projected population growth, wage growth, modal mix and purpose of travel in cities, and how these might evolve. From the bottom up, we considered the light/heavy traffic mix on specific roads, proportion exposed to WFH and traffic distribution throughout the day, and how this might change. This also included ongoing monitoring of traffic data released by companies and tracking indicators such as congestion, travel speed and user mobility data published by the likes of TomTom, INRIX, Apple and Google to keep re-examining our views on what might happen over the medium and longer term.

Wind forward the clock two years and many of these questions and concerns are no longer relevant. Tough pandemic restrictions have significantly receded following a global rollout of vaccines 12 months ago, with many measures having completely disappeared. Road volumes have returned.

Airport share prices have rebounded strongly from pandemic lows on the so-called ‘recovery trade’, in some cases returning to pre-pandemic levels. Toll road total returns remain more subdued. This is despite road volumes in many parts of the world having returned to ‘normal’, with some roads experiencing traffic and congestion above pre-COVID levels. While not the case universally, it does provide a strong indication that many of the concerns in 2020 about the potential for permanent impairment of toll road assets were overblown and greatly exaggerated.

We believe investor behaviour has a part to play in the underperformance of toll roads. The old adage “shoot first, ask questions later” drove a key part of the initial selloff and subsequent underperformance of road assets in the rebound.

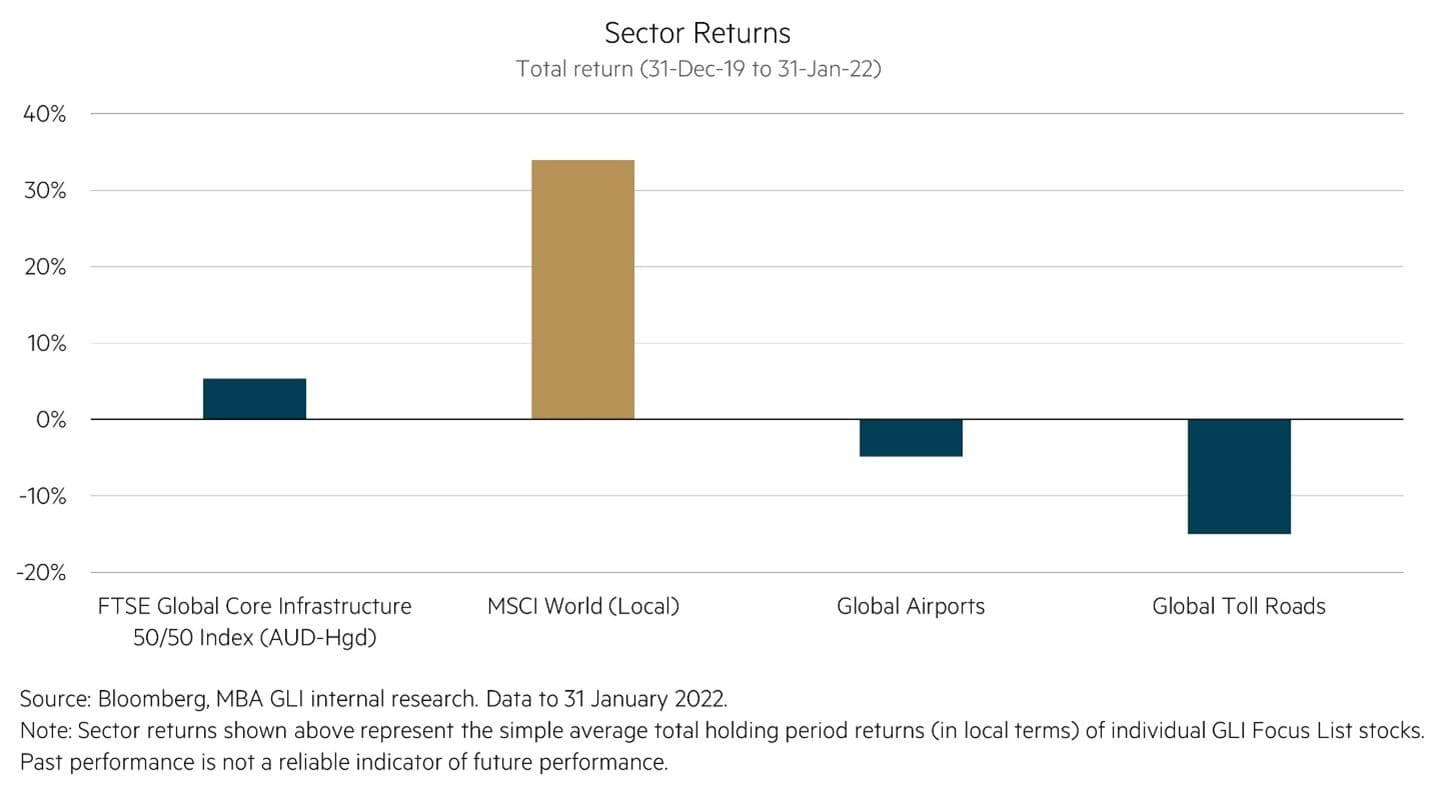

The average airport company’s total return has been negative 5% since 2019. The average toll road company’s return is approximately negative 15% and remains the worst infrastructure sub-sector since the pandemic began. Fundamentals suggest it should be the other way around. Over the same timeframe, the infrastructure asset class as a whole is up about 5% on a local/hedged basis, and global equities is up about 35%. Is the market telling us that investors think a 50% relative performance differential between toll roads and global equities is reasonable?

It is here where we have found new portfolio opportunities. Australian investors would be very familiar with Transurban – but there are many other excellent toll road opportunities for investors scouring the globe. Over the past two years, we have significantly increased our portfolio exposure to toll roads assets – from only 8% at the end of 2019 to about 17% today. This includes the addition of three new toll road holdings, including Ferrovial as a top 5 position, which was not even owned in the portfolio in 2019.

Toll roads are unique assets to invest in – not only are they typically very long duration, they are natural monopolies with limited capital expenditure once constructed and often described as ‘cash cows’. They are also relatively easy businesses to model with typically transparent structures and clear commercial frameworks driving revenues and cash flows.

In an environment where investors are worrying about the threat of increasing inflation and rising rates, it is natural to be cautious of longer duration assets. Long bond yields have bounced back to pre-pandemic levels, yet the share price remains well below, something we believe to be incongruous when fundamentals have normalised. We also believe many of these assets are also some of the best pricing-power monopolies that money can buy – many with embedded inflation escalators, that is, raising tolls with prevailing inflation rates quarterly or annually. Some roads actually have dynamic pricing power. Evidence of this inflation link has continued to come through. Also, road traffic is often linked to GDP, which provides a volume growth offset to higher discount rates from rising rates in an expanding economy.

In a prior article on Livewire, What inflation means for this defensive, high-yielding asset class, we discussed strong inflation protection is a key attribute of the infrastructure asset case. Toll roads play a leading role here.

Fundamentals and stock-picking are starting to matter after the past two years of pandemic headlines and macro-driven markets. Road volumes and congestion have mostly normalised, and despite the somewhat consensus concerns of rising interest rates, we believe toll roads are now in the hot seat.

Disclaimer

This material was prepared by Maple-Brown Abbott Ltd ABN 73 001 208 564, Australian Financial Service Licence No. 237296 (MBA). MBA is registered as an investment advisor with the United State Securities and Exchange Commission under the Investment Advisers Act of 1940. This information is intended solely for professional and institutional investors and is provided for information purposes only. This material is not intended for, and is not suitable for, retail clients and does not constitute investment advice or an investment recommendation of any kind and should not be relied upon as such. This information is general information only and it does not have regard to any investor’s investment objectives, financial situation or needs. Before making any investment decision, you should seek independent investment, legal, tax, accounting or other professional advice as appropriate. This material does not constitute an offer or solicitation by anyone in any jurisdiction.

This material is not an advertisement and is not directed at any person in any jurisdiction where the publication or availability of the information is prohibited or restricted by law. Past performance is not a reliable indicator of future performance. Any comments about investments are not a recommendation to buy, sell or hold. Any views expressed on individual stocks or other investments, or any forecasts or estimates, are point in time views and may be based on certain assumptions and qualifications not set out in part or in full in this information. The views and opinions contained herein are those of the authors as at the date of publication and are subject to change due to market and other conditions. Such views and opinions may not necessarily represent those expressed or reflected in other MBA communications, strategies or funds. Information derived from sources is believed to be accurate, however such information has not been independently verified and may be subject to assumptions and qualifications compiled by the relevant source and this material does not purport to provide a complete description of all or any such assumptions and qualifications. To the extent permitted by law, neither MBA, nor any of its related parties, directors or employees, make any representation or warranty as to the accuracy, completeness, reasonableness or reliability of the information contained herein, or accept liability or responsibility for any losses, whether direct, indirect or consequential, relating to, or arising from, the use or reliance on any part of this material. This information is current as at the date of publication and is subject to change at any time without notice.

We use a tight definition of infrastructure assets with low-volatility cashflows and inflation protection to achieve diversification benefits with other asset classes, such as global equities.