Media release

2 min

Looking at the recent divergent country results across emerging markets highlights why investors should not view them as a homogenous block. There are almost always opportunities for investors. By the end of the September 2022 quarter, global emerging markets had crossed into the longest bear market since the MSCI EM Equities index creation in 1988 (590 days and -40% from the February 2021 peak). Emerging market valuations of 10.3x forward earnings are at levels last seen through the lows of the COVID meltdown and very close to previous lows of the past 10 years. That said, the outlook for those forward earnings is under pressure. We see opportunities with the fall in valuations but remain cautious on the outlook for broader market moves and wary of further cuts to earnings estimates. Two markets, China and Brazil, illustrate challenges along with opportunities of investing in emerging markets.

In a broad market fall of 12.5% for the quarter, the standout negative contributor was China at -23%. Back in March 2022, there appeared to be capitulation in the Chinese market as large cap companies like Tencent fell 30% in the space of a few weeks. Market commentary was that China was “uninvestable”. That is usually the sign of a market bottom, and there was some stabilisation through the June quarter. However, through September the China market reached new lows.

In our opinion, the initial sell-off in China from the market peak in February 2021 was driven by a clampdown on the big technology platforms and a focus on redistributing wealth to lower income households (the drive for ‘common prosperity’). However, consumer confidence is now the drag.

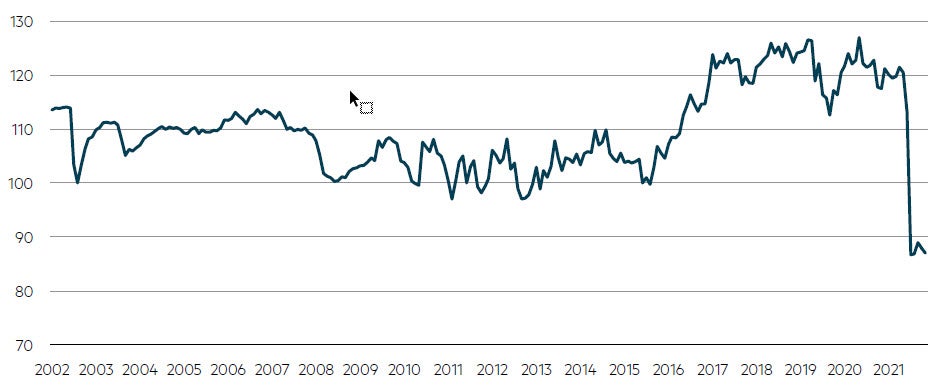

China consumer confidence at all-time lows

Source: China National Bureau of Statistics, data to 31 August 2022.

Surveys of consumer confidence in China have hit all-time lows. Behind this is the ongoing COVID restrictions, with China maintaining a zero-COVID policy. However, these were in place already. We believe the key driver is the weak housing market (according to China’s Academy of Social Sciences, housing represents 45% of the wealth of Chinese households). This weakness is driven by the central government’s desire to bring property developers’ debt levels under control. In August 2020, the government introduced the “three red lines” policy that restricted lending to developers if their debt was deemed to be unsustainable. This led to the default of Evergrande in December 2021. While Evergrande defaulting did not cause the system itself to collapse, it damaged the confidence of real estate buyers. This confidence issue is even more relevant in China where the structure of the real estate market is for buyers to pay 100% upfront for their unbuilt apartment and maintain a mortgage for one or maybe two years before they even have the apartment. The logical next step then, if buyers are concerned on the viability of their property developer, is not make the initial purchase or even stop making mortgage payments. This restricts a vital funding source for property developers, which hits their traded bonds, which reinforces the questions around the viability of their business model as their cost of borrowing soars.

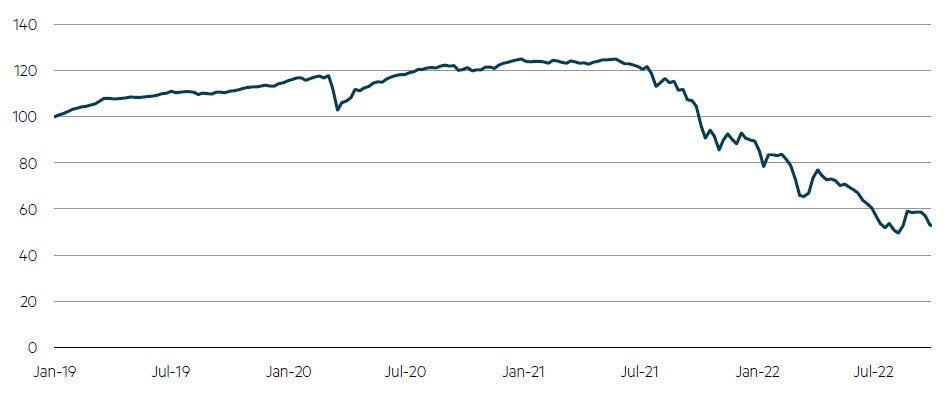

China Property Developers USD Bond Index

Source: CRIC, Bloomberg, data to 30 September 2022

We believe there is a way out of this. The government has been reluctant to offer mass bailouts and move away from its focus on debt reduction in the system. We have seen incremental moves, such as lowering mortgage rates, but this does not solve the confidence issue, which is now needed. Recent initiatives are moving in this direction. The government has offered credit default guarantees for select developers, created a RMB300 billion fund for developers to complete stalled housing projects and on 30 September, according to Bloomberg, the six largest banks were directed to offer at least RMB600 billion in lending to the real estate sector by the end of 2022. The potential for stability in the housing market could be enough to restore consumer confidence and attract investors back to Chinese equities.

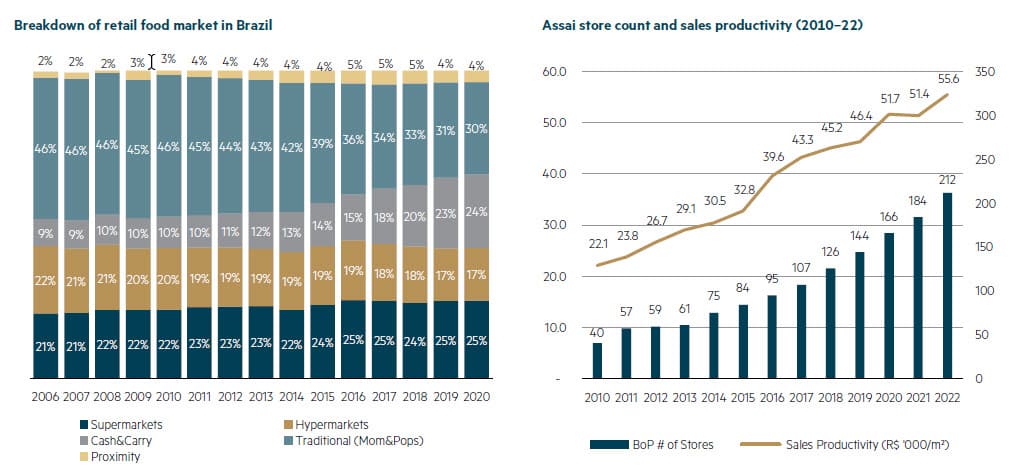

On the positive side for the September quarter, Latin America as a region returned +2% against the broader emerging markets of -12%. Within that, Brazil gained 8% and was home to the largest contributor in the portfolio for the quarter – Sendas Distribuidora. Sendas Distribuidora, better known by its brand name, Assai, is the largest pure play cash and carry retailer in Brazil, with 234 stores mainly in the wealthy states of Sao Paolo and Rio de Janeiro.

We like the business model of discount supermarkets. Assai has consistently been highly cash generative with negative working capital and cash flow returns on invested capital around 30%. In an environment of higher inflation and squeezed consumer budgets, we would expect consumers to move towards this lower-priced format. Over time, Assai sales have proven to grow ahead of inflation. At the same time, Brazil has plenty of room for the cash and carry format to grow in the years ahead. A common theme across emerging markets is the large share of traditional retail, which is being replaced by the mass consumer moving to more formal shopping. In recent years in Brazil, cash and carry has gained market share from hypermarkets and traditional retailers, and we would expect this trend to continue.

Left – Source: Credit Suisse, Euromonitor, 5 December 2021 | Right – Source: Assai company data, Maple-Brown Abbott, 28 July 2022

Assai does not come risk-free. It is 41% held by a highly indebted parent, Casino Group of France, with market fears the parent company will force the highly cash generative Assai to buy assets from, or even lend cash directly to, the parent. In fact, it is this overhang and a purchase of stores by Assai that created the opportunity for us to enter Assai at attractive valuations and benefit from the reduction in that perceived overhang. As Assai rebrands and rolls out those purchased stores, we expect a lift in earnings and even an increase in levels of cash returns on capital. The Assai management team has previously achieved this in turning around other store purchases from the parent company. We continue to see attractive levels of upside in Assai, but with the outperformance, our expected total rate of return has reduced to about the portfolio average.

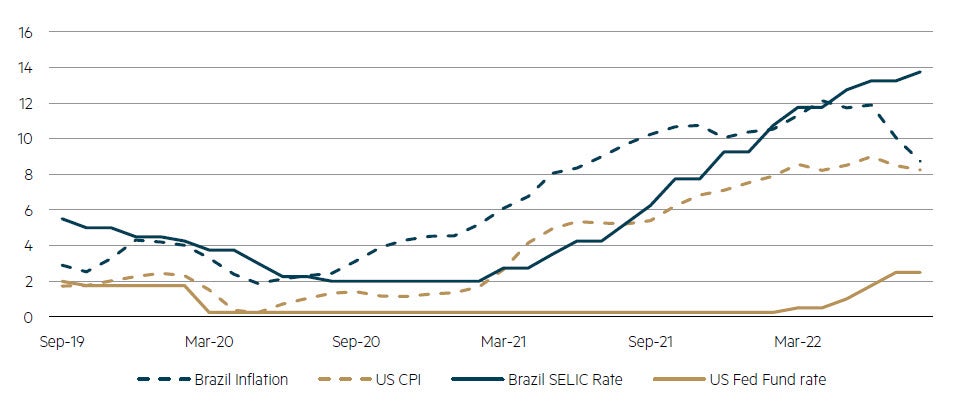

As a market, Brazil is trading on 7x forward PE and has a central bank that has been well ahead of the curve on inflation. The SELIC rate (Brazil’s base interest rate) has been increased from 2% in February 2021 to 13.75% in August 2022. Clearly memories of hyperinflation run deep with these bankers. Consumer price inflation in Brazil has already peaked at 12% year over year, with the latest reading at 8.7% year over year, leading to positive real interest rates (see chart below). This leaves room for the central bank and government to stimulate if required. Additionally, through October Brazil worked through the overhang of a general election. The election went to a second round between the left leaning Lula of the PT party and right leaning Bolsonaro of the PL party. Ultimately, Lula was victorious, and Bolsonaro has agreed to abide by the constitution and begin the transition of power. Aside from removing an overhang (which is usually a positive itself), the conclusion of a close election was taken positively as both sides on the left and right have had to moderate their views to attract endorsements and ultimately, voters. At these market valuations, we continue to find attractive upside to ideas in the country.

Brazil tightening 12 months ahead of developed markets

Source: FactSet, Maple-Brown Abbott, data to 31 August 2022.

Despite the short-term market moves and our cautious outlook, we believe a number of long-term trends such as the emerging market mass consumer offer opportunities to investors. We also believe a portfolio of well-run businesses with sustainable business models that are generating high cash returns on capital and purchased at a substantial discount to our estimate of fair value will outperform over the long term.

Disclaimer

This information was prepared and issued by Maple-Brown Abbott Ltd ABN 73 001 208 564, Australian Financial Service Licence No. 237296 (“MBA”). This information must not be reproduced or transmitted in any form without the prior written consent of MBA. This information does not constitute investment advice or an investment recommendation of any kind and should not be relied upon as such. This information is general information only and it does not have regard to any person’s investment objectives, financial situation or needs. Before making any investment decision, you should seek independent investment, legal, tax, accounting or other professional advice as appropriate. Past performance is not a reliable indicator of future performance. Any comments about investments are not a recommendation to buy, sell or hold. Any views expressed on individual stocks or other investments, or any forecasts or estimates, are point in time views and may be based on certain assumptions and qualifications not set out in part or in full in this information. The views and opinions contained herein are those of the authors as at the date of publication and are subject to change due to market and other conditions. Such views and opinions may not necessarily represent those expressed or reflected in other MBA communications, strategies or funds. Information derived from sources is believed to be accurate, however such information has not been independently verified and may be subject to assumptions and qualifications compiled by the relevant source and this information does not purport to provide a complete description of all or any such assumptions and qualifications. To the extent permitted by law, neither MBA, nor any of its related parties, directors or employees, make any representation or warranty as to the accuracy, completeness, reasonableness or reliability of the information contained herein, or accept liability or responsibility for any losses, whether direct, indirect or consequential, relating to, or arising from, the use or reliance on any part of this information.

Interested in investing with us?

Focusing on the impact of cyclical and structural change on companies, we use a rigorous and repeatable process to construct a concentrated portfolio which captures the opportunities offered by the dynamic nature of emerging markets.