The beginnings of 2024 saw a continuation of the 2023 market trends: India and Taiwan strength, while China continued to fall. Forced selling in Mainland exchanges was triggered by derivative product losses (’snowballs’) and added to the already weak sentiment. Biotech companies also came under pressure as US legislators looked to implement new measures that limited future growth.

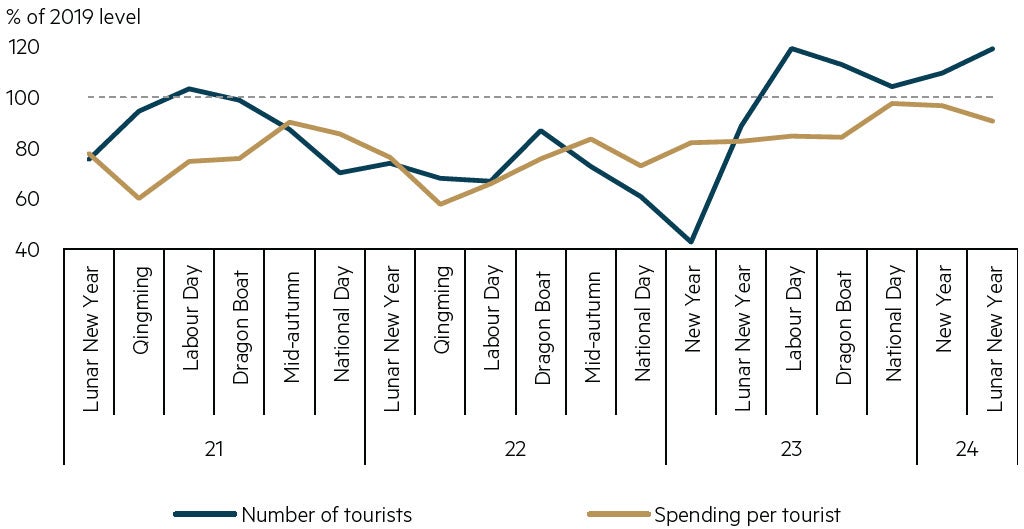

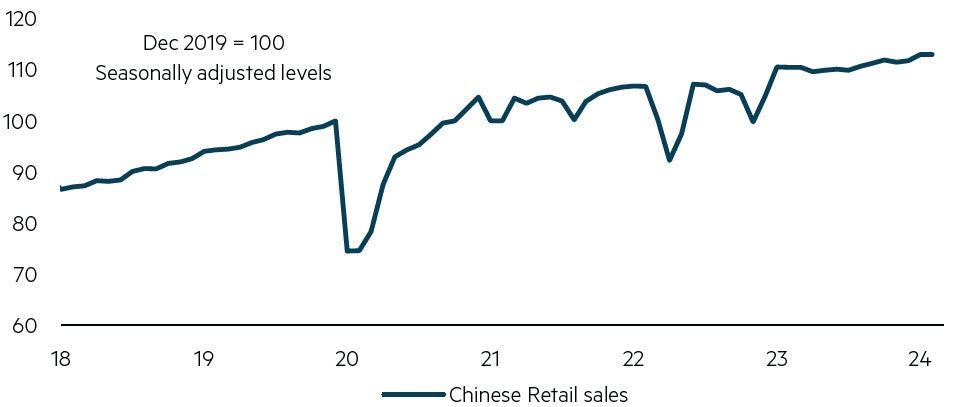

Markets rallied in February with better data out of China confirming the underlying reality: China’s economy continues to recover. As shown in the first chart below, tourist numbers over the Lunar New Year period were above 2019 levels. The second chart below shows retail sales are growing at mid-single digits, while the government is targeting GDP growth of “around 5%” in 2024.

Signs of recovery 1: Domestic tourism in China

Source: Macquarie Bank. Data as at March 2024.

Signs of recovery 2: Retail sales in China

Source: Macquarie Bank. Data as at February 2024.

Admittedly it is slower than what markets had expected coming out of COVID and China’s economy still faces challenges, with falling property prices and its beleaguered property development industry being chief among them. We note that government policy is actively addressing these issues and is starting to find traction. Whether this proves to be the bottom for equity markets in China remains to be seen, but there are reasons to be optimistic. Cheap valuations, low investor positioning, better capital returns and an ongoing economic recovery - it has many ingredients for contrarian opportunity.

Capital returns in Asia – Japan, China and South Korea leading the way

Japanese equity markets were one of the strongest performing in 2023, and during the recent quarter the most quoted benchmark (Nikkei 225) surpassed its previous all-time high set back in December 1989! A significant driver of the strength in markets has been improving corporate governance. While this has been a process that dates back to reforms first implemented back in 2014, specific measures implemented by the Tokyo Stock Exchange in early 2023 have essentially forced companies to improve their corporate governance, payout excess cash and thereby increase share prices.

Japan’s success has not gone unnoticed in South Korea. Given their shared history, similar growth models and common industries they compete in, what happens in corporate Japan has ramifications in South Korea. Over the quarter, the Financial Services Commission (FSC) announced its own plan, called the Corporate Value-Up Program (‘Value-up’). First discussed in late January, the FSC shared further guidelines in late February (with specific details to be shared in June).

The guidelines announced in February centre on three pillars:

- Increasing transparency and disclosure. Encouraging and supporting voluntary disclosure around individual company value-up plans, along with (unspecified) incentives to participate in the program.

- Promoting companies that follow best practice. Authorities plan to establish a “Korea Value-up Index”, comprising companies with proven records of profitability or those anticipated to do so under the program. An ETF will also be established so retail investors can gain access to these companies.

- Ongoing regulatory support. A longer-term department to be established, dedicated to the Value-up program and making improvements over time.

South Korea has been an alluring destination for value-oriented investors for many years. The country is home to a number of world class companies (as well as a few dominant local ones) which often trade at a discount to their international peers. Despite the attractive valuations, it has also been a source of frustration for investors as a multitude of factors ranging from weak corporate governance, tax laws and overzealous regulators have prevented that value from being realised. Hence the Value-up program has garnered significant investor attention since it was announced.

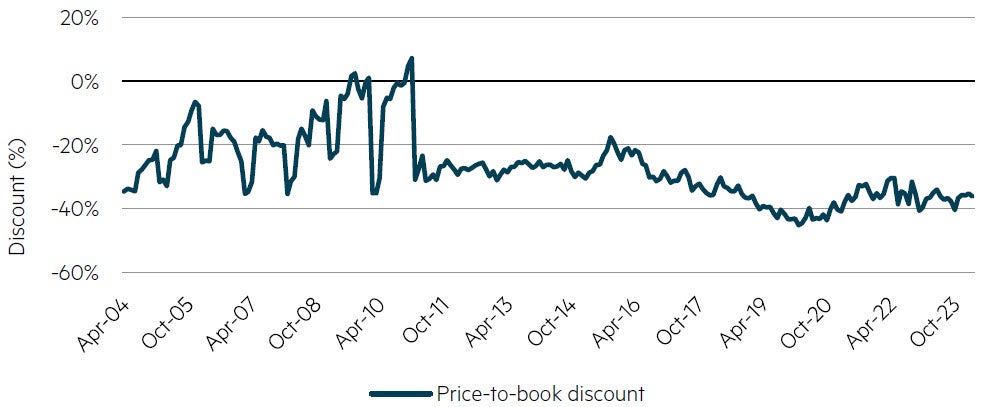

The Korea Discount: Kospi price-to-book versus Asia ex Japan price-to-book

Source: FactSet. Data to March 2024.

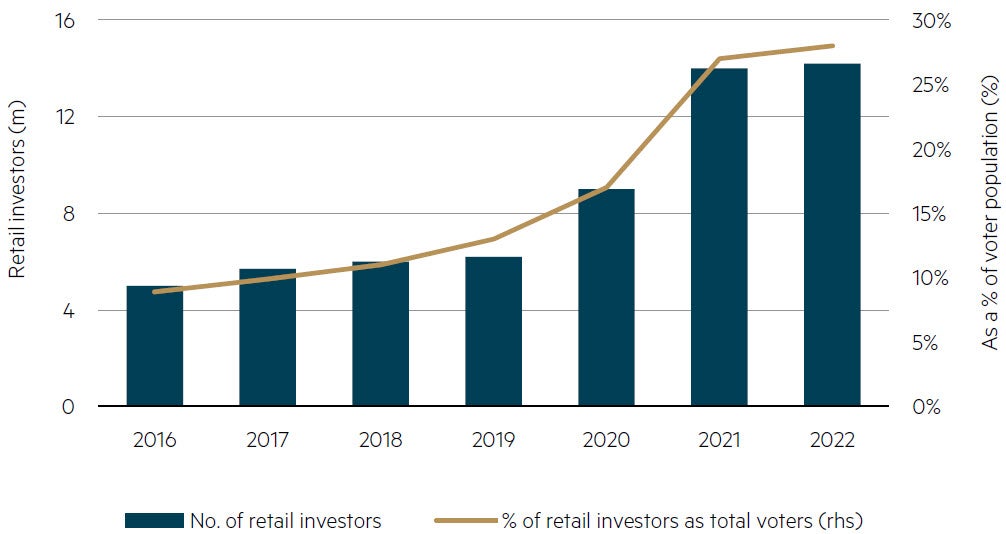

Long term investors in the region may look upon the recent developments with cynicism and ask: why now? Certainly, the success of Japan’s program is a factor. However, there is another reason closer to home. The rise of the retail shareholder in Korea has accelerated since President Yoon won office in 2019. At that time, around 12% of voters were invested in the stock market, however this number has more than doubled to ~27% to the end of 2022 (see below). In November last year, a ban on short selling in Korean equities was introduced, as well as a reduction in capital gains tax. The legislative elections held in early April were a near-term setback for President Yoon, with the opposition party winning the election. Despite this development, it will be difficult to reverse the direction of corporate governance reform, however areas like more aggressive tax reform that may have accelerated change will be harder to implement. This is an important consideration of the program as inheritance as well as dividend tax rates are onerous relative to comparative countries. Controlling families have an incentive to keep dividends low and share prices depressed in order to minimise these taxes. The voluntary nature of the program has also been a disappointment to some. Yet with a rising retail shareholder voting class and the success of neighbouring programs, we expect these reforms to continue to take shape over the coming months.

The Rise of the (Voting) Retail Shareholder

Source: KSD, Goldman Sachs. Data to December 2022.

Process in action: Hyundai Mobis

Portfolio holding Hyundai Mobis (Mobis) is a good example of better capital allocation potentially leading to a material uplift in its share price. The company is part of the Hyundai Motor Group and manufactures auto parts, primarily for Hyundai and Kia vehicles. This part of the business is well placed to manage the transition to electric vehicles, as it primarily consists of components that remain relevant in an EV world (braking systems, power steering, airbags etc). It also has a highly profitable after-sales parts business, linked to the growing fleet of Kia and Hyundai cars globally. Finally, it also owns a 21% stake in Hyundai Motor (as part of a series of cross holdings across the three companies) that accounts for ~45% of its current market cap. The company is cash rich, with around US$5bn in net cash on balance sheet, accounting for ~29% of its market cap. Despite these valuable assets, the company’s valuation remains extremely low: trading on a PE ~6x 2025 and 0.5x of its book value.

Activist investors had targeted Mobis in the past and had some success, with the company initiating a buyback several years ago. Our analysis indicates it can do substantially more while still funding its ambitious capital expenditure plans. Restructuring of the broader group is a complex affair given cross holdings, inter-generational ownership transfer and the related tax issues, however with newfound political support the value in Mobis (as well as the wider South Korean market) is closer to being realised than ever.

Similar reforms in China

Meanwhile, with much less market attention, reforms have also been taking place in China. Initially aimed at state owned enterprises (SOEs) at the Central government level, more recent measures are seeing private enterprises being impacted. The first signs of reform started in January 2023 when the state assets regulator (SASAC) announced the introduction of Return-on-Equity as a metric for management performance. Many SOEs are cash rich which depresses return on equity, meaning management teams looking to boost return on equity can easily pay out excess cash via dividends and/or buybacks. Portfolio holding Kunlun Energy is a good example of this phenomenon. At its 2023 results it increased its dividend and guided to higher payouts going forward. Moreover, with approximately one third of its market cap in cash, it has the ability increase dividends for many years to come.

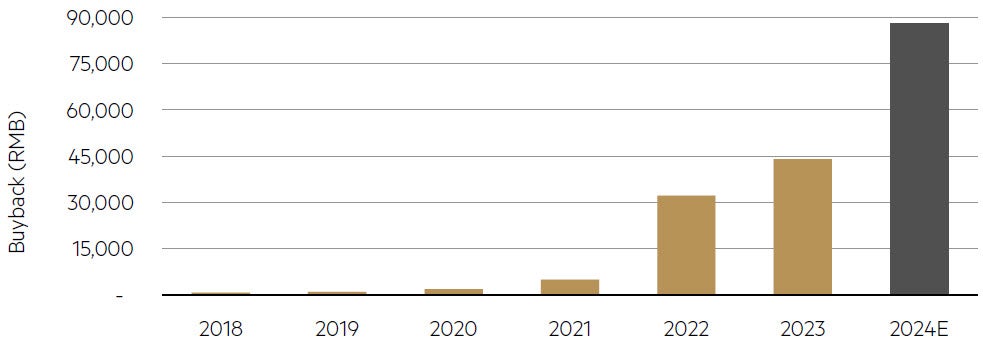

Dividend and buyback surprises were a key feature in the recent reporting season in China. Overall, dividends per share expectations were 12% higher than expected (for those companies that had reported by 31 March) and several large companies announced significant buybacks*. Importantly, number of internet related companies also announced significant buybacks: Tencent said it would double the level of its buyback to RMB 100bn in 2024, while Alibaba also upped its buyback program to ~US$35bn (~18% of its market cap) over the next three years. Meanwhile NetEase increased its payout ratio on its quarterly dividend to 75% (from 30%).

Stock repurchases at Tencent are ramping up

Source: Company data, MBA estimates as at March 2024.

More recently, SASAC expanded its key performance indicators to include SOE market value (i.e. share price) as a measure. This addresses a long-held criticism of these companies in China. While the practical implementation of this new measure is unclear at this stage, we note the simple fact that SOEs being (partly) measured on their share price performance demonstrates considerable progress.

Meanwhile, Chinese authorities replaced the head of the CSRC (market regulator) in February. New head Wu Qing spoke at China’s Two Sessions in early March and specifically addressed the importance of good corporate governance, as well as supply side issues including de-listings and reducing the number of IPOs.

Parting thought

It is an often-overlooked fact that of the total return from the Asia ex-Japan region over the past 20 years, around half has come from dividends. With strong balance sheets and generally low payout ratios, better capital allocation (via returning more cash to shareholders) has the potential to both increase returns as well as substantially re-rate the market. The developments during the quarter are another positive step in this regard, which continue to be in the early stages and importantly, not being priced in by the market.

* Source: Bloomberg, March 2024.

Disclaimer

This information is prepared and issued by Maple-Brown Abbott Ltd ABN 73 001 208 564, AFSL. 237296 (‘MBA’) as the Responsible Entity of the Maple-Brown Abbott Asian Investment Trust ARSN 102 593 457 (‘Fund’). This article contains general information only, and does not take into account your investment objectives, financial situation or specific needs.

Before making a decision whether to acquire, or to continue to hold an investment in the Fund, investors should obtain independent financial advice and consider the current Product Disclosure Statement and Target Market Determination (TMD) or any other relevant disclosure document which are available at maple-brownabbott.com/document-library or by calling 1300 097 995.

Any views expressed on individual stocks or other investments, or any forecasts or estimates, are not a recommendation to buy, sell or hold, they are point in time views and may be based on certain assumptions and qualifications not set out in part or in full in this document. Information derived from sources is believed to be accurate, however such information has not been independently verified and may be subject to assumptions and qualifications not described in this document. To the extent permitted by law, neither MBA, nor any of its related parties, directors or employees, make any representation or warranty as to the accuracy, completeness, reasonableness or reliability of this information, or accept liability or responsibility for any losses, whether direct, indirect or consequential, relating to, or arising from, the use or reliance on this information. This information is current as of 29 April 2024 and is subject to change at any time without notice.

© 2024 Maple-Brown Abbott Limited.