Research paper

8 min

Webcast: Asian equities – March 2021

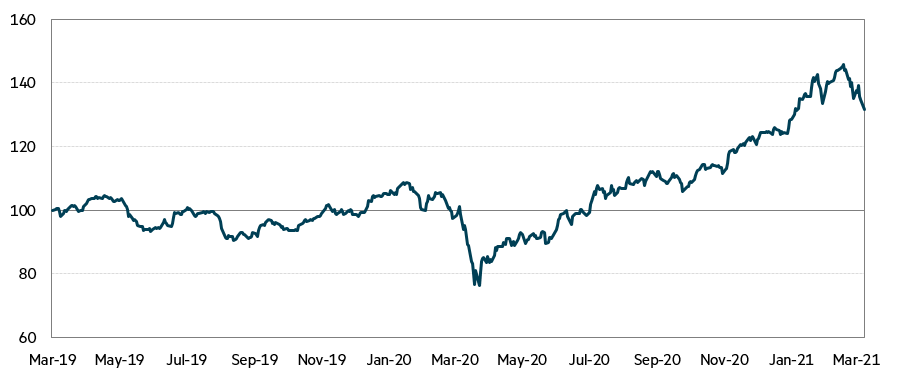

As we approach the first anniversary of the nadir in markets caused by the COVID-19 induced sell-off, it is remarkable to look at what has changed since then as well as reflect on what has not. From the January peak to the March lows last year, the regional benchmark declined 30% (in USD’s), a familiar pattern observed elsewhere in the globe that represented one of the sharpest and most pronounced drawdowns in history[1]. At the time many argued that such moves were a proportionate, if not inadequate, response to a global setback of a scale not observed since the second world war. Perhaps less anticipated was the war-like response by governments and central banks across the globe with their monetary and fiscal programs. The record stimulus combined with the news last November of the success of several vaccine trials further unleashed animal spirits among investors in the truest Keynesian sense. From those March lows the MSCI AC Asia ex-Japan benchmark has rallied an impressive 80% (in USD’s), rendering the shape of the recovery more akin to the Nike ‘swoosh’ than the much-discussed V!

MSCI AC Asia ex-Japan benchmark: Recovery shape more like the Nike ‘swoosh’ than a V

Source: FactSet data to February 2021.

From our portfolio’s perspective, we have seen a welcome improvement in relative performance. Since last November our Asia ex-Japan strategy has returned 33.9%[2] versus the benchmark’s 21.6%[3]. The stimulatory forces, coupled with the concomitant increase in bond yields, have underpinned a sharp rotation towards the value cohorts of the market that had long been out of favour.

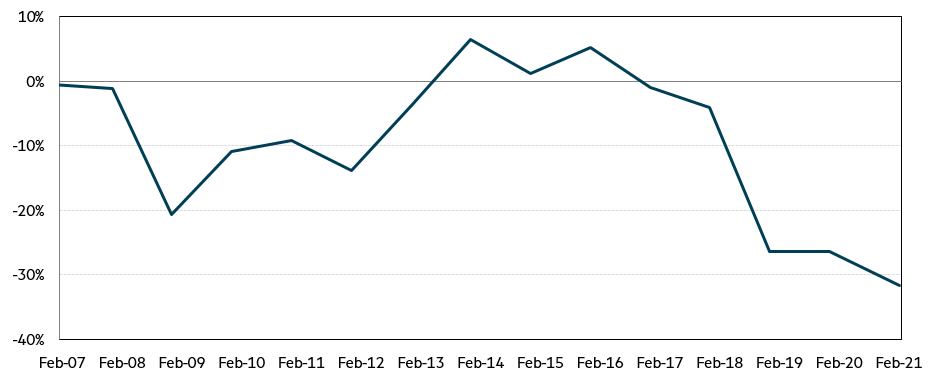

As an example, sectors such as financials, commodities and auto companies that in many instances were trading at record discounts to market have all rallied very strongly, with a number of portfolio holdings gaining more than 50% in barely four months. Two of our key holdings, Baidu and State Bank of India, have doubled over this period. In our view, these holdings still resemble reasonable value and are trading below their historic long-term metrics. As shown in the accompanying chart, despite the recent bounce, on an aggregate basis our portfolio continues to convey a significant discount to the market in terms of its forward Price Earnings Multiple (PE). As a consequence of our value positioning the portfolio is less exposed to the negative impacts from a higher cost of equity being imputed from increasing bond yields.

Portfolio PE discount to the market*

Source: MBA, data to February 2021.

We have long written about the unjustifiable de-coupling we had observed between the sound underlying fundamentals of many of our portfolio holdings and their prevailing share prices. In that context, it is certainly pleasing, though not surprising, that investors are showing greater interest in these parts of the market given the improved confidence surrounding their earnings outlook.

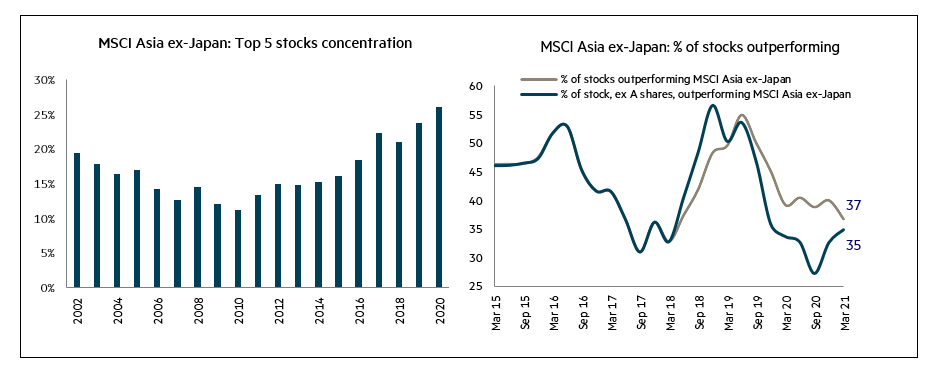

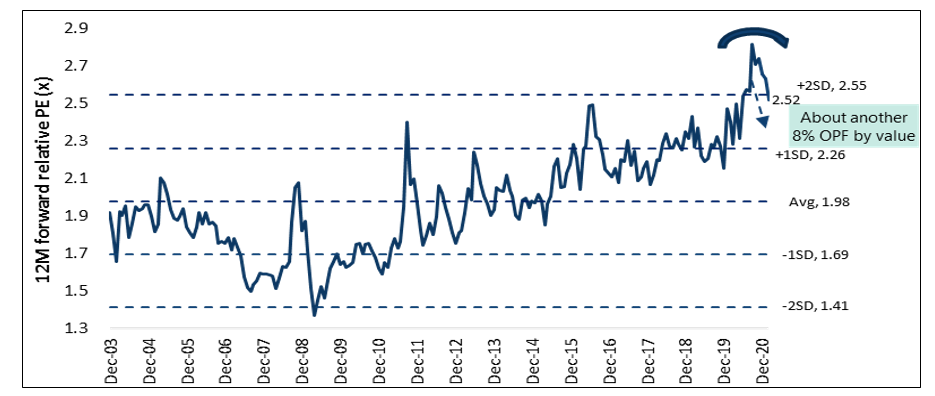

Only time will tell if the sharp rotation of recent months heralds the end of the winter endured by value investors or is simply a temporary burst of sunshine. There is no doubt that the recent recovery in value and subsequent sell-off in bonds has given those pundits proclaiming ‘the death of value’ cause to reflect. As highlighted in the following charts, despite some early rotation, the weight of money remains herded toward a narrow group of very large stocks and richly priced stocks suggesting a potential rotation remains in its infancy.

Source: FactSet, CLSA. Data as at 4 March 2021.

MSCI Asia ex-Japan Growth (Quality) vs Value Relative PE

Source: Jefferies, data as at 4 March 2021.

Despite the relatively nascent change in sentiment, it is interesting how quickly the narrative has changed among the myriad of strategists and market commentators. Advocating a value strategy is fast becoming the consensus recommendation among many of them. Storied value investor Seth Klarman once noted that “you don’t become a value investor for the group hugs”. Perhaps we are about to enjoy the warm embrace of the consensus after all.

In summary, although volatility has increased, generally both fixed income and equity markets have followed a relatively orthodox pattern in recent months consistent with a reflationary outlook for global growth. It is salutary to remember that what is now considered an ‘elevated’ yield on the US 10-year treasury bond of 1.5% was in fact a fresh record low less than five years ago. With central banks around the world seemingly intent on keeping the monetary pedal flat to the floor and with real rates still firmly in negative territory, the ‘normalisation’ of interest rates may continue for some time yet. We believe our portfolios remain well-positioned to continue to benefit from a synchronised global recovery. We look forward to providing a more detailed update on both the value renaissance and our underlying portfolio in our March quarterly report.

Author

Geoff Bazzan

The Asian region rewards research, patience, discipline and experience. We have been investing in the region for 20 years, following companies and countries through different cycles to gain a deeper understanding of the risks and rewards.